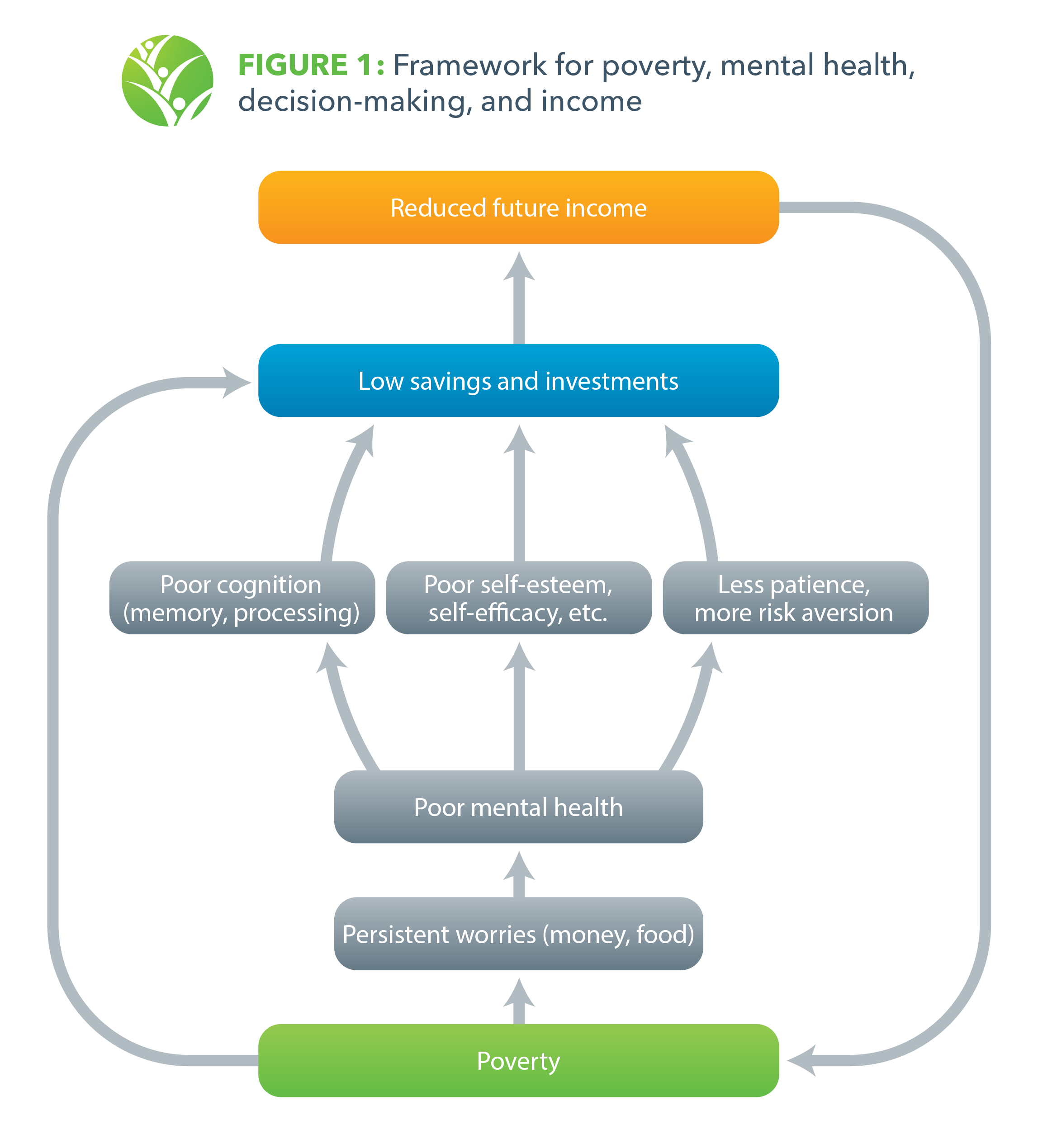

In new research, we outline how the relationships between poverty and mental health are mediated by aspects of psychological well-being that affect forward-looking decision-making. There are several pathways studied in the literature for how poor mental health can constrain forward-looking behavior:

- Poor cognitive function—stress affects the brain’s short-term memory and the ability to carry out complex tasks.

- Reduced patience—feelings of anxiousness lead people to focus on immediate threats rather than long term goals.

- Low self-esteem—those with lower self-esteem may fall back on default options, have difficulty choosing among a large number of options, or avoid making decisions.

- Higher risk-aversion—possible negative consequences may feel dire for forward-looking decisions that entail risk.

These problems reduce the ability to make optimal and timely decisions that could help households transition out of poverty. When people can process information well and recall a full range of potential options, they are able to make better decisions. People tend to save and invest more when they are more patient because they give more weight to future plans. Higher self-esteem leads to more confidence and decisiveness, and lower risk-aversion means that people make more potentially higher return investments (e.g. in new agricultural technologies).

Figure 1 depicts these relationships, illustrating how, because of these negative reinforcing processes, the poor can end up in psychological poverty traps. But on the positive side, these relationships also imply that providing resources to poor households may help them escape those same traps. A growing literature shows that social protection—in particular, direct cash transfers to the poor—is a particularly promising approach in this regard.

In an accompanying IFPRI discussion paper, we study the effects of a cash transfer program on psychological well-being and investment behavior in Mali, where poverty rates are high and mental health resources are low. We evaluate the effects of Mali’s national cash transfer program, Filets Sociaux (Jigisémèjiri), taking advantage of the program’s randomized phase-in design. Jigisémèjiri began in 2014 and was designed to serve the population’s lowest income quartile, which experiences chronic food poverty. The program provided unconditional transfers of 10,000 West African CFA francs (about $18) per month, delivered every quarter over three years—amounting to approximately 13% of beneficiaries’ pre-program income in the sample we analyze. Transfers were bundled with accompanying measures that that included messaging around using the transfer for savings and investment.

For our impact evaluation, we use baseline data collected just prior to the program’s start, and follow-up data collected when “treatment” households had been receiving program benefits for approximately two years and “control” households had not yet started participating. Our analysis traces out the steps outlined in Figure 1, looking at psychological well-being outcomes of the main decision-maker in the household. (We focus on stress/anxiety as the survey did not measure depression.)

For the first step in the cycle—persistent worries about money/food—we find that the cash transfer program led to an 11% reduction in worry about both money for basic expenditures and worry about having sufficient food. In a context in which 69% of people report being worried about having enough food, this is a meaningful effect. We also find that the program leads to a reduction of 8% in a broader measure of stress/anxiety, representing the second step. The results are mixed for the next step. We find that the transfers substantially raise a measure of self-esteem. In companion qualitative work, one male household decision-maker explained that the transfers made him feel that he could provide for his family, an important source of pride for him. There are also suggestive increases in measures of patience—decision-makers indicate being slightly more willing to wait for a higher amount of money in the future vs. receiving a lower amount now. We find no significant impacts on our measures of cognition.

Lastly, for the fourth step relationship, we look at household savings and investments. We find that households that received the program were more than twice as likely to have savings, make more investments in the previous 12 months, and consequently, own 21% more productive assets. The investments were made in productive assets such as livestock, small animals, and non-agricultural equipment, all of which can contribute to income-generating activities and a diversification of income sources. Livestock can also act as a form of savings; households in settings similar to Mali often sell off livestock when they experience a shock and need liquid cash.

It is worth noting that, while cash transfers had positive impacts on some areas of psychological well-being and investments, we cannot necessarily conclude that the former is responsible for all impacts on the latter. Simply having more income can directly affect investments and assets, as reflected by the arrow in Figure 1 between poverty and investment/savings. Our ongoing work attempts to disentangle these relationships.

Nonetheless, our initial findings show that cash transfer programs can improve not only immediate income and other economic outcomes, but also psychological well-being outcomes, which are important in and of themselves. We should recognize these additional benefits as an important part of the overall impact of cash transfer programs, and as a promising approach to improving psychological well-being in settings where this might help households escape poverty.

Melissa Hidrobo and Shalini Roy are Senior Research Fellows with IFPRI’s Poverty, Health, and Nutrition Division (PHND); Naureen Karachiwalla is a PHND Research Fellow.

Support for this research was provided by the Government of Mali and the IFPRI-led CGIAR Research Program on Policies, Institutions, and Markets (PIM).

We thank Francisco Barba, Bastien Koch, and Leila Njee-Bugha for excellent research assistance, and also thank the participants of this study.